Homeownership Pathway

Rent or Buy a Home in Canada: What’s Better for Newcomers?

Homeownership Pathway

Is Home Co-ownership a Solution for Newcomers to Canada?

Homeownership Pathway

Can Newcomers Rent-to-Own a Home in Canada?

Join the Scotiabank StartRight® Program designed for Newcomers‡ and get up to $2,300* in value in the first year.

Written By

Corinna Frattini

Feb 28, 2025

•Homeownership Pathway

For many newcomers buying your first home is a source of pride, satisfaction, and accomplishment! And, buying a home is an investment that grows over time and provides a great financial benefit. But before jumping in, consider these vital first-time home buyer tips!

Buying your first home is expensive and likely the biggest purchase you make in your lifetime. Buying a house in Canada may be different than in your home country from the process to the types of homes, styles, layouts, materials, and costs. Understanding first-time home buyer basics will help you make the right decision.

Take advantage of free tools and resources to research the housing market before you buy a home. Learn about housing price trends, affordability, and mortgage rates. Researching before you buy a home will help you make a confident decision.

You can use online mortgage calculators that give you approximate costs, and monthly mortgage payments.

You can talk to your lender about getting a pre-approved mortgage certificate.

There are many different real estate companies in Canada and agents to choose from.

A real estate lawyer will review your purchase agreement contract. The wording in these contracts is important and your lawyer will ensure everything is done properly in terms of the law.

Plan for your home closing costs or the costs associated with the date you take possession of your home.

Many newcomers arrive in Canada with savings to buy their first home. A 2019 survey conducted by Royal LePage revealed that newcomers represent a growing segment of the Canadian real estate market. Some of the findings showed that newcomers:

It makes sense that newcomers are eager to enter the housing market in Canada. Indeed, owning your own home is exciting for many reasons. Homeownership can be a great investment and a way to build personal wealth. Young families may want more space with a backyard for children to play. Or, buying a home in Canada may be an important part of your immigration dream!

But rarely do people have enough money to buy a house outright. This is where lenders can help you by giving you a loan, also known as a mortgage. But, you will need enough savings to pay for a down payment before you can get approved for a mortgage.

Essentially, a down payment is a portion you put down towards the value of your home right up front. You subtract the down payment from the home purchase price and supplement the remaining cost with a mortgage. You may have to build your savings if you don’t have enough for a down payment.

In addition to saving money for a down payment, there are other costs to pay such as closing costs. It’s important to factor in the closing costs because they can be expensive and often take first-time homebuyers by surprise. So before you rush into buying a home, it’s important to understand all the costs involved for a first-time home buyer in Canada.

If you have recently arrived in Canada, you’ll discover many exciting things in the city you have landed in. You may love the city and want to make it your home. On the other hand, you may learn that it’s not quite what you had expected. Or, you may land a job in a different city and want to relocate to another region or city in Canada. When you first arrive in Canada, it’s best to continue renting until you’re certain where you want to live long-term. Resettling is expensive.

Renting a home versus buying a home makes sense if you:

A large advantage of buying a house is the sense of pride that comes from owning your home in Canada. In addition, you become a part of a community where you know your neighbours and gain a sense of belonging. And most importantly, you’ll gain financial benefits when you:

In general, it makes sense to buy a home if you plan to remain in the city for five years or more.

Before becoming a first-time homebuyer, you must prepare to meet new financial obligations. These are three important steps to take before you buy a home:

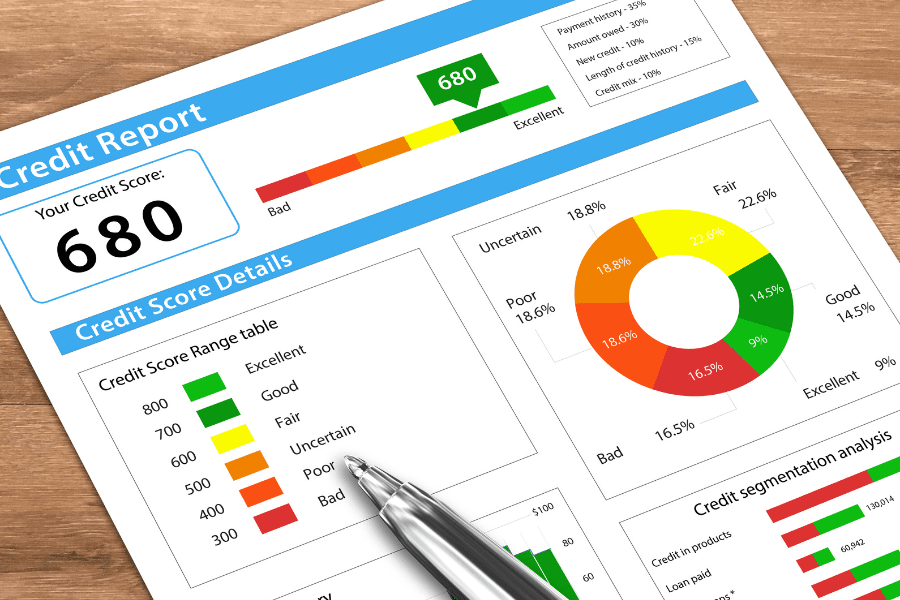

When buying a house as a newcomer, you must build your credit history in Canada. You can build credit by applying for a credit card or a small loan and making regular payments.

Most importantly, you need to save for your down payment. However, you can own your home in Canada with as little as just a five percent down payment and mortgage insurance.

Another important requirement for first-time home buyers is financial stability. You need financial discipline when you buy a home. For example, save money for an emergency fund for unexpected expenses such as a leaky roof, basement flooding, or a burst pipe. Any of these expenses could cost thousands of dollars.

The minimum down payment in Canada is the percentage of the home’s purchase price. And depending on the house price, the minimum down payment amounts vary.

For example, the minimum down payment is:

Until you have enough money for the down payment, continue to rent.

In addition to thinking about financial first steps, you’ll also need to consider other practical questions such as:

As a guideline, financial experts state that you should not pay more than 30% – 35% of your total household income for housing and home-ownership costs such as:

But, that’s a guideline. You may decide to budget more for housing or, cut back on other expenses such as entertainment or dining out.

A mortgage pre-approval means that a lender has stated that you qualify for a mortgage loan based on your current income and credit history. The pre-approval will indicate the:

The lender will assess your financial situation and determine how much they are willing to lend. This will give you confidence when choosing which homes to consider buying. It will also help when you make an offer on a property because the buyer knows you are serious and able to purchase.

When you’re ready to search for a home, you need to consider:

With answers to these questions, you can narrow your search to find the ideal home for your needs. You can also provide this information to your realtor who can help you find your ideal home in Canada. Realtors are trained and licensed to help you find and buy a resale property. You may choose an agent who has sold other properties in the areas that you are considering. Or, you may choose a realtor that a friend or family member recommends.

Talk to the realtor about the important things to you in a home, but keep a realistic approach. Many Canadians buy a starter home” and then work their way up the property ladder. Be ready to accept that your price range may not cover all the features you want in a house.

You do not pay for the services of a realtor. Realtors earn a commission on the home’s selling price. The home seller pays the commission, not the buyer.

Once you’ve found a property you want, you’ll want to make an offer. An offer represents your desire to purchase the property and the amount you’re willing to pay. Your real estate agent can advise on the price you should offer on a resale home based on your local market conditions and recent home sales in the neighbourhood.

After agreeing on a price, the seller will stop showing the property to other prospective buyers because the home is now ‘conditionally sold’ to you, and will begin to take the necessary steps to complete the transaction.

Similarly, you will also need to begin taking steps to fulfill your part of the purchase process, including any conditions you may have listed in your offer such as a home inspection or finalizing financing. These vary by location, and your realtor is a good person to ask about the next steps.

Typically, the offer-to-purchase agreement will include:

This is a detailed description of the residence’s address, including street name, house, lot, and block number. It will also often include a list of additional items included in the sale (appliances, garage door openers window coverings, etc).

Here a clearly-stated purchase price that both parties have deemed acceptable will appear. There will also be a description of the deposit amount here. A deposit demonstrates that you are serious about your offer, and will persuade the seller to not entertain any further offers. The Offer will also often contain the payment method (cheque, credit card, etc.), as well as mention who will hold the deposit.

This is when the property becomes yours and you can move in. By this time, any previous owner is expected to have removed all of their belongings and cleared any of the conditions you may have imposed.

Typically, the seller is responsible for the property until the closing date and guarantees that they have the legal right to sell the property. They also guarantee that all buildings and improvements do not encroach upon neighbouring lands.

This is where you place any changes or improvements to the property that the seller and buyer agree to.

This is where you’ll typically find a list of agreed-upon conditions of sale, the breach of which could result in a nullification of the purchase agreement. This could include a description of financing conditions, property inspection conditions, condominium documents conditions, and the sale of buyer’s home conditions.

In addition to your mortgage, there are several closing costs that you must pay before you can take possession of your house. To “take possession” means the home is now legally yours. First-time home buyers are very often surprised when they learn of these additional costs. Examples of closing costs that you can expect to pay include:

This is the cost for an appraiser to assess the property value. Your mortgage lender may require an appraisal to determine whether the selling price is reasonable for the market.

You must pay the Goods and Service Tax (or Harmonized Sales Tax) on a newly constructed or substantially renovated home. Resale homes do not require a GST payment.

This tax is charged to buyers in most provinces, usually based on the purchase price.

This includes fees charged by your lawyer for services such as conducting a title search, drafting a title deed, and preparing the mortgage, and registration fees. A guideline for costs is typically between 1.5% to 4% of the purchase price of the home.

High-ratio mortgages (those with less than 20% down payment) require mortgage default insurance. The cost is usually added to the mortgage it varies depending on the amount of your down payment.

Special insurance coverage to cover the cost of your mortgage in the event of death or severe illness is available from most lenders.

Hiring a home inspector is voluntary but recommended for resale homes, and usually, the cost ranges from $400-$600. With a home inspection, you may discover issues with the house that will cause you to back out of your offer. Or, the home issues may be manageable and you could ask for a lower purchase price to offset any repair expenses.

You may want to bring in an electrician, plumber, and perhaps a structural specialist to ensure you understand all the home systems. They can also provide cost estimates for repairs if needed. First-time home buyers may not factor in these additional costs.

When you buy a house, a home inspection is critical. Usually, an offer to buy a home is conditional upon an inspection. An inspection will assess the following areas:

Foundation: an inspector will check if there is a leak in a foundation wall and whether insulation is in place. If there’s an active leak, they will determine the condition behind the wall.

Plumbing: the inspector will determine if the drains are installed properly and not leaking.

Windows: the inspector will ensure window seals are not damaged. For example, if one of the windows gets fogged, that tells that the window has to be replaced. Next, the home inspector will look at the frame to see if any openings must be resealed; otherwise, you may get an air leakage.

Furnace: the home inspector will check the quality of the filter and whether it is installed properly. They will check the quality and age of the furnace and whether it’s leaking any water inside or gas, which could be critical.

Mold: an inspector will also look for mold (or termites) in the house because it can result in significant costs to repair later.

When buying a house in Canada consider these vital first-time home buyer tips. Learn the essentials and become informed about everything that’s involved. Homeownership provides great pride, security, and achievement. The more informed you are, the more confident you’ll be about your home purchase decisions!

WRITTEN BY

Corinna Frattini

Senior Editor and Content Writer, Prepare for Canada

Corinna researches and writes content to help newcomers make informed decisions about housing, employment, banking, and aspects of settling in Canada. With a background in human resources and leadership development, her articles focus on how newcomers can continue their careers in Canada. Her writing combines research, practical guidance, and clear language to support newcomers on their journey.

© Prepare for Canada 2026

Rent or Buy a Home in Canada: What’s Better for Newcomers?

Is Home Co-ownership a Solution for Newcomers to Canada?

Can Newcomers Rent-to-Own a Home in Canada?